How much do Polish renewables actually earn?

A MWh of solar in Poland earns 283 PLN; a MWh of wind earns 414 PLN; the market average is 448 PLN. This post uses capture price and capture factor as tools to track how those numbers have moved since 2020, why wind and solar diverge, and what that means for project economics.

TL;DR

- In 2025, Polish solar captured only 283 PLN/MWh, while wind captured 414 PLN/MWh; the demand-weighted market average was 448 PLN/MWh.

- On a per-MW basis, that means about 310 kPLN/MW/year for solar versus 1,040 kPLN/MW/year for wind, assuming 1100 full-load hours for solar and 2500 for wind.*

- Since 2021, the gap has widened: solar has been increasingly exposed to midday price cannibalisation, while wind has retained a stronger capture profile.

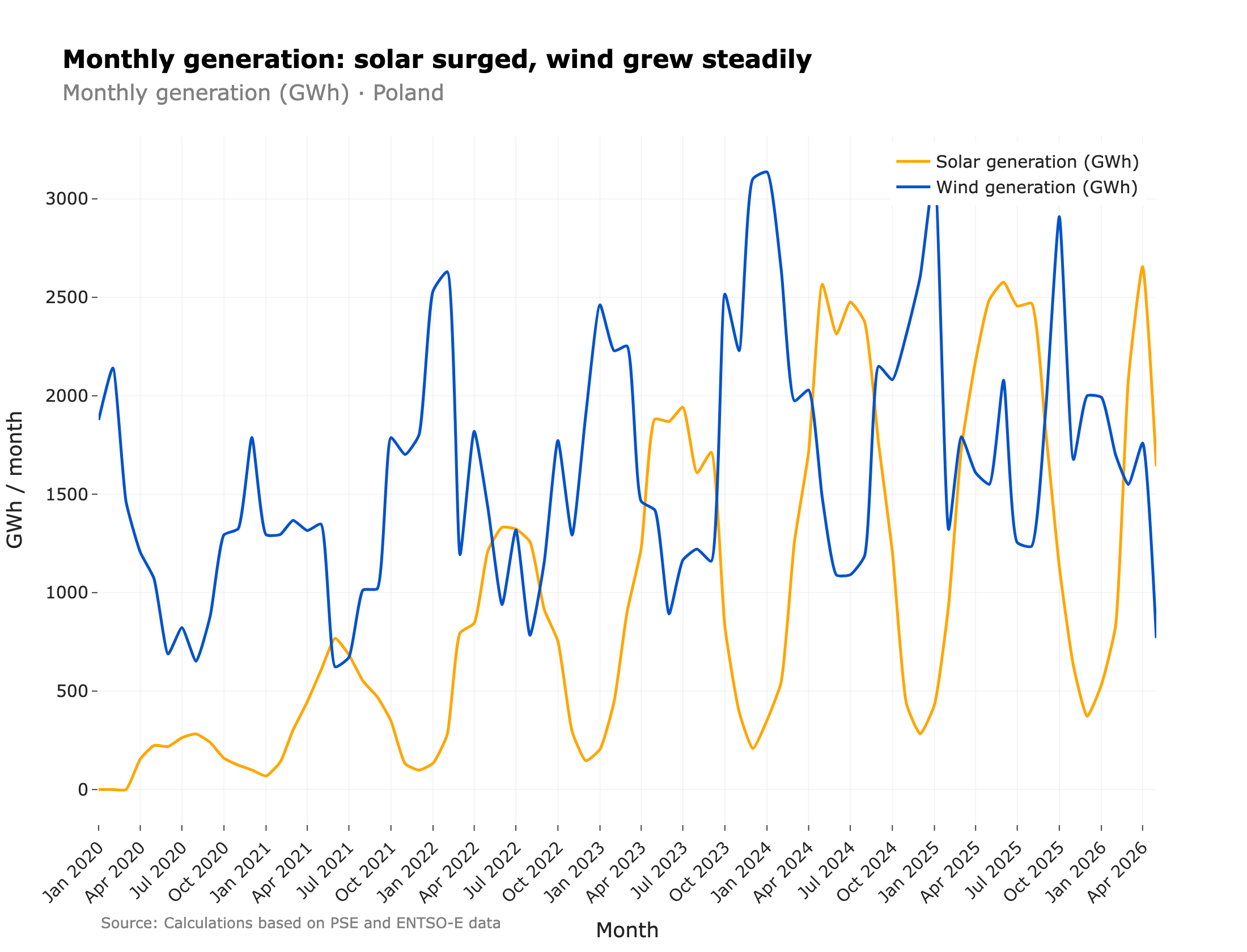

Solar and wind generation

Let’s start with a quick overview of how solar and wind generation have evolved in Poland over the last few years. The chart below shows monthly generation for both technologies.

Solar and wind generation have been steadily increasing over the last couple of years. Both technologies show seasonal variability, with solar peaking in the summer months and wind generating the most in winter, which has a positive effect on the system. At a daily level, wind generation is inversely correlated with solar generation — very windy days rarely coincide with high solar generation. Days with both low wind and low solar are not that rare, though, which I described in this post.

The share of total RES generation in Poland increased from 12.3% in 2021 to 26.1% in 2025, with solar being the main contributor to that growth.

It is not surprising that such growth has an impact on the power system and market dynamics, which is what I will explore in the next sections.

| Year | Solar generation | Wind generation | Share of total generation |

|---|---|---|---|

| 2021 | 4.61 TWh | 15.24 TWh | 12.3% |

| 2022 | 9.29 TWh | 18.77 TWh | 17.3% |

| 2023 | 13.22 TWh | 22.11 TWh | 23.1% |

| 2024 | 17.29 TWh | 23.78 TWh | 26% |

| 2025 | 19.23 TWh | 22.49 TWh | 26.1% |

Table 1: Annual solar and wind generation in Poland and their combined share of total generation, 2021–2025. Source: own calculations based on PSE / ENTSO-E data.

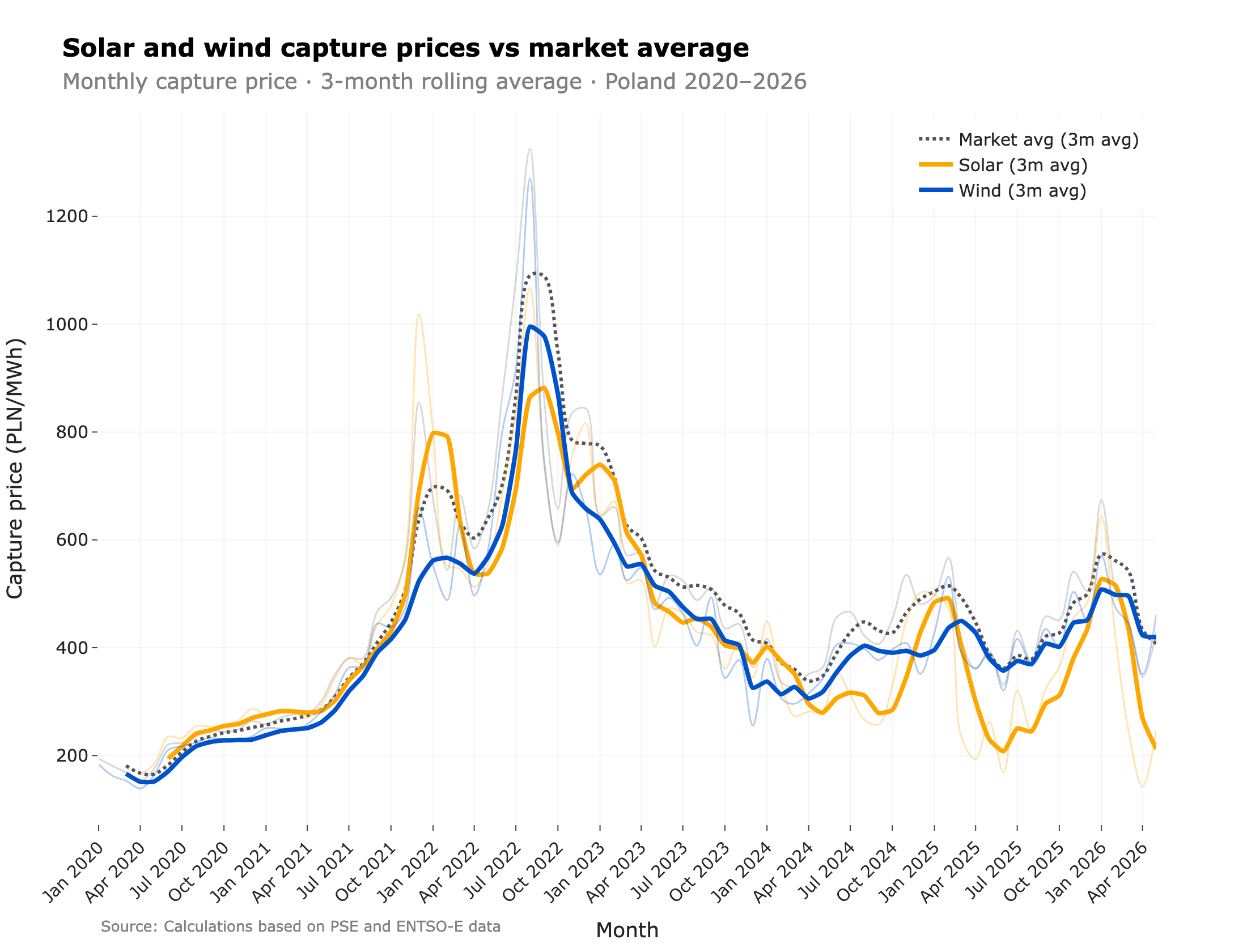

Capture price

To estimate how much a solar or wind installation would earn over a given period, say a year, we need to know how much energy it generated and at what price. The amount of energy is straightforward to estimate from weather data and installed capacity, but what about the price? That’s where capture price comes in.

Capture price is one of the metrics used to measure the worth of energy generated by a given technology. We need such a metric because the value of a MWh depends on when it is generated — a MWh generated at 7pm on a sunny day is worth more than one generated at 3am, and non-dispatchable sources generate unevenly through the day. Capture price reflects this time-varying value by taking the average price a technology receives, weighted by how much it generated in each hour.

Where is the price in hour and is the generation in hour .

It’s handy because it gives a single number that summarizes the value of a technology’s generation, and it can be compared to the market average to see if the technology is earning a premium or a discount.

Capture prices since 2020

The chart above shows how wind and solar capture prices have evolved in recent years, with the dotted lines marking the market average. Prices are low and stable in the early part of the chart, then jump sharply in 2022 (the energy crisis), followed by a period of elevated and more volatile prices since 2024.

Let’s focus on the period from 2024 onward, as it is more representative of the current situation. Wind capture price is more stable and trending slightly upward, while solar capture price swings widely from winter highs to summer lows.

| Year | Solar capture price | Wind capture price | Market avg |

|---|---|---|---|

| 2020 | 235 | 194 | 214 |

| 2022 (peak) | 714 | 651 | 796 |

| 2025 | 283 | 414 | 448 |

Table 2: Solar and wind capture prices vs demand-weighted market average in Poland, selected years (PLN/MWh). Source: own calculations based on PSE / ENTSO-E data.

Why the absolute number isn’t enough

- 2022 capture prices were high because the market was high (gas crisis), not because the generation profile improved.

- To strip out market-wide moves and compare across years, the ratio matters more than the level — that’s the capture factor.

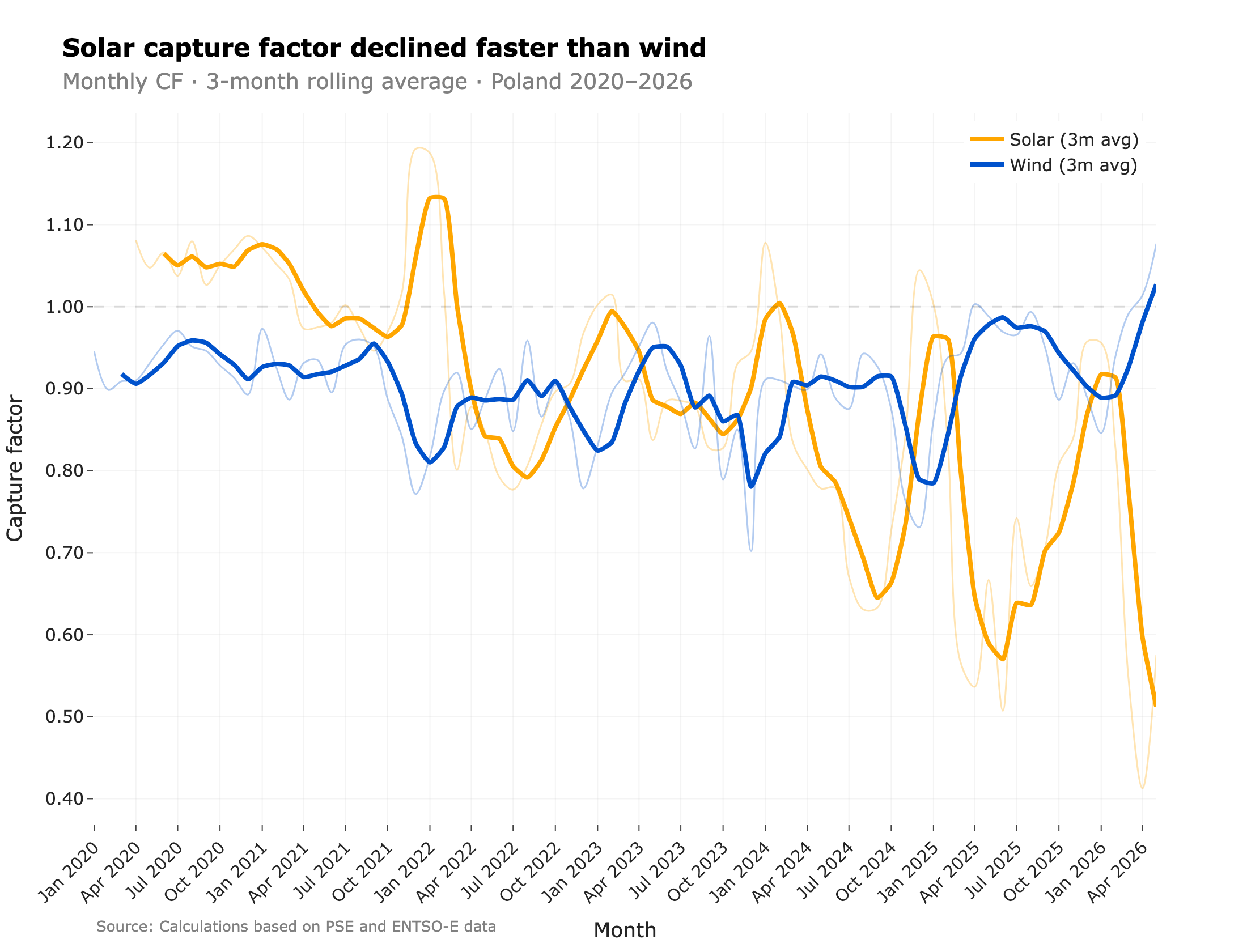

Capture factor

Capture price is useful to understand how much a technology earns in absolute terms. In order to understand how it performs relative to the market, we can use the capture factor, which is the ratio of the capture price to a reference market price.

- A capture factor of 1.0 means the technology earns the average market price.

- Below 1.0 means it earns a discount; above 1.0 means it earns a premium.

Capture factor is useful because it strips out market-wide price moves and lets us compare a technology’s relative performance across different time periods. For example, if the market price doubles but the capture price also doubles, the capture factor stays the same, telling us the technology’s relative performance hasn’t changed.

How the picture has changed since 2020

There are a couple of things we can see in the chart above:

- Solar and wind capture factors tend to move in the opposite direction: the lower solar’s capture factor, the higher wind’s — and vice versa. This can be seen as a sign of the solar-induced price profile being beneficial for wind, which can sell part of its energy at higher prices in the evening hours.

- Wind capture factor tends to slightly increase over time, with the spring months of 2026 being even above 1.0. Solar capture factor, on the other hand, has been on a steady decline since 2021, with the gap to the market average widening significantly in 2023. The lows appear lower each year starting from 2023. In April 2026, the capture factor fell to around 0.41.

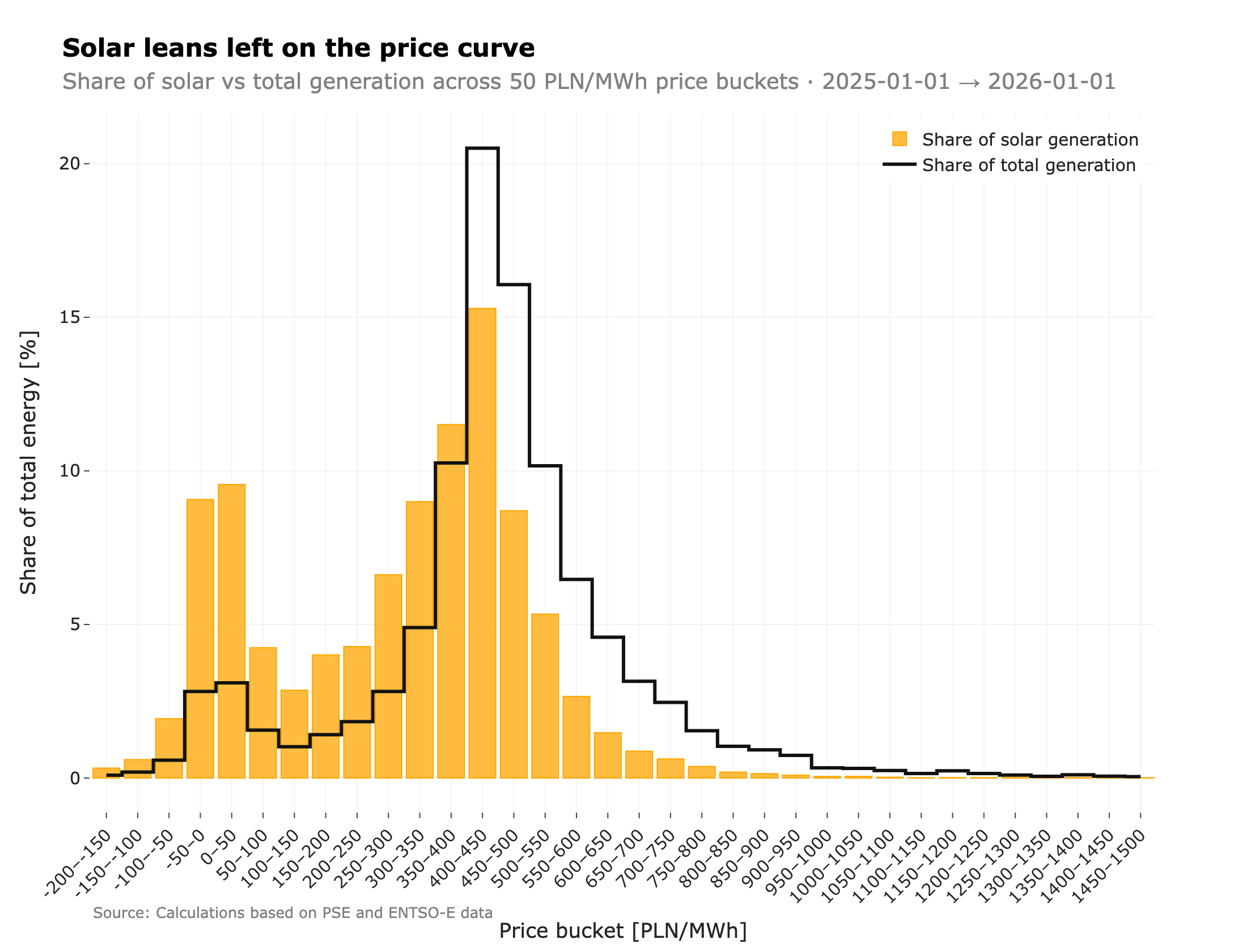

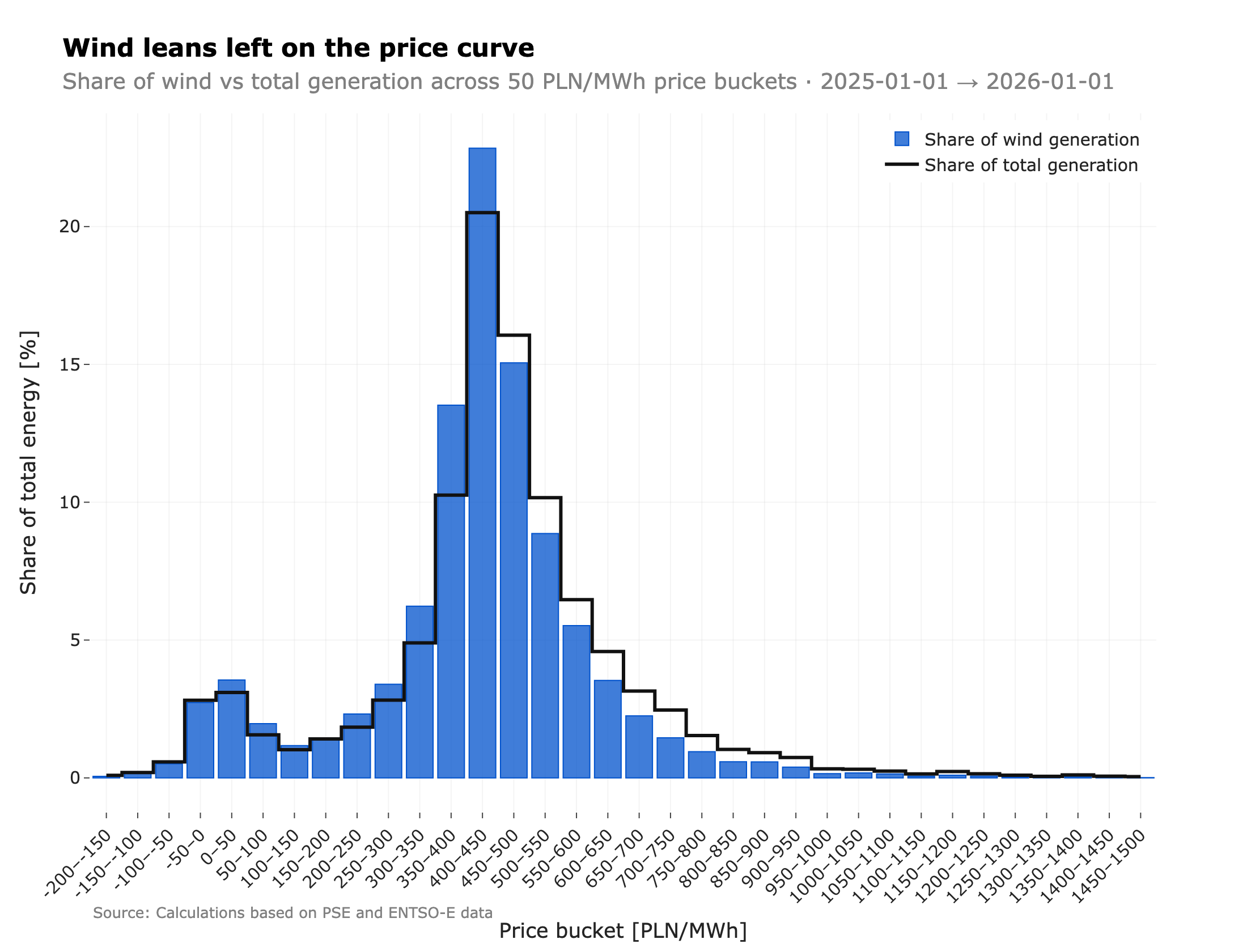

Where on the price curve renewables sit

Aggregate view: where each MWh lands

This is a visual representation of the capture factor. If solar and wind had a capture factor of 1.0, their generation distributions would match the total generation distribution (line). Instead, solar is heavily skewed towards low-price buckets (left side), while wind is more evenly distributed — also leaning towards lower prices, but much less than solar.

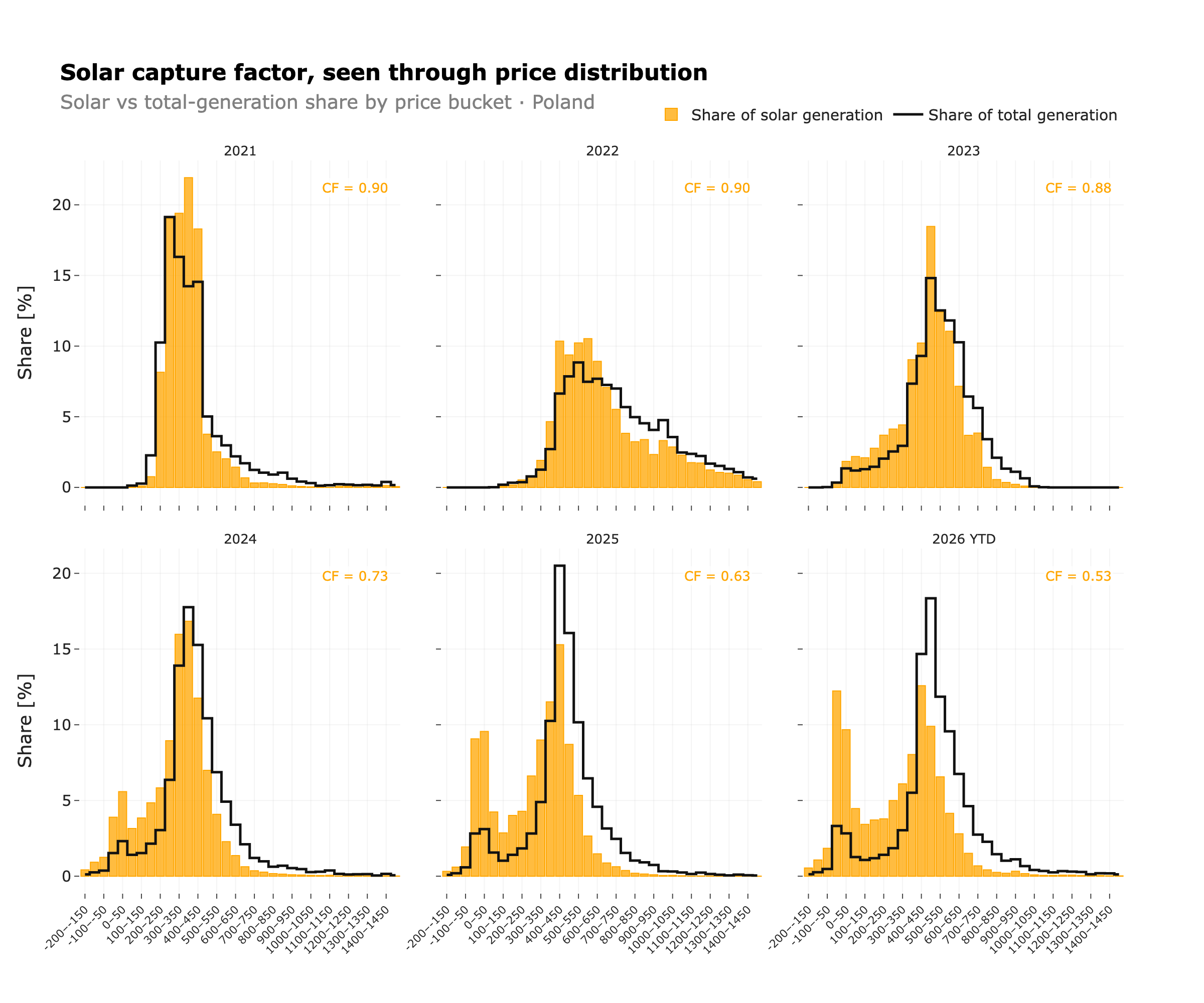

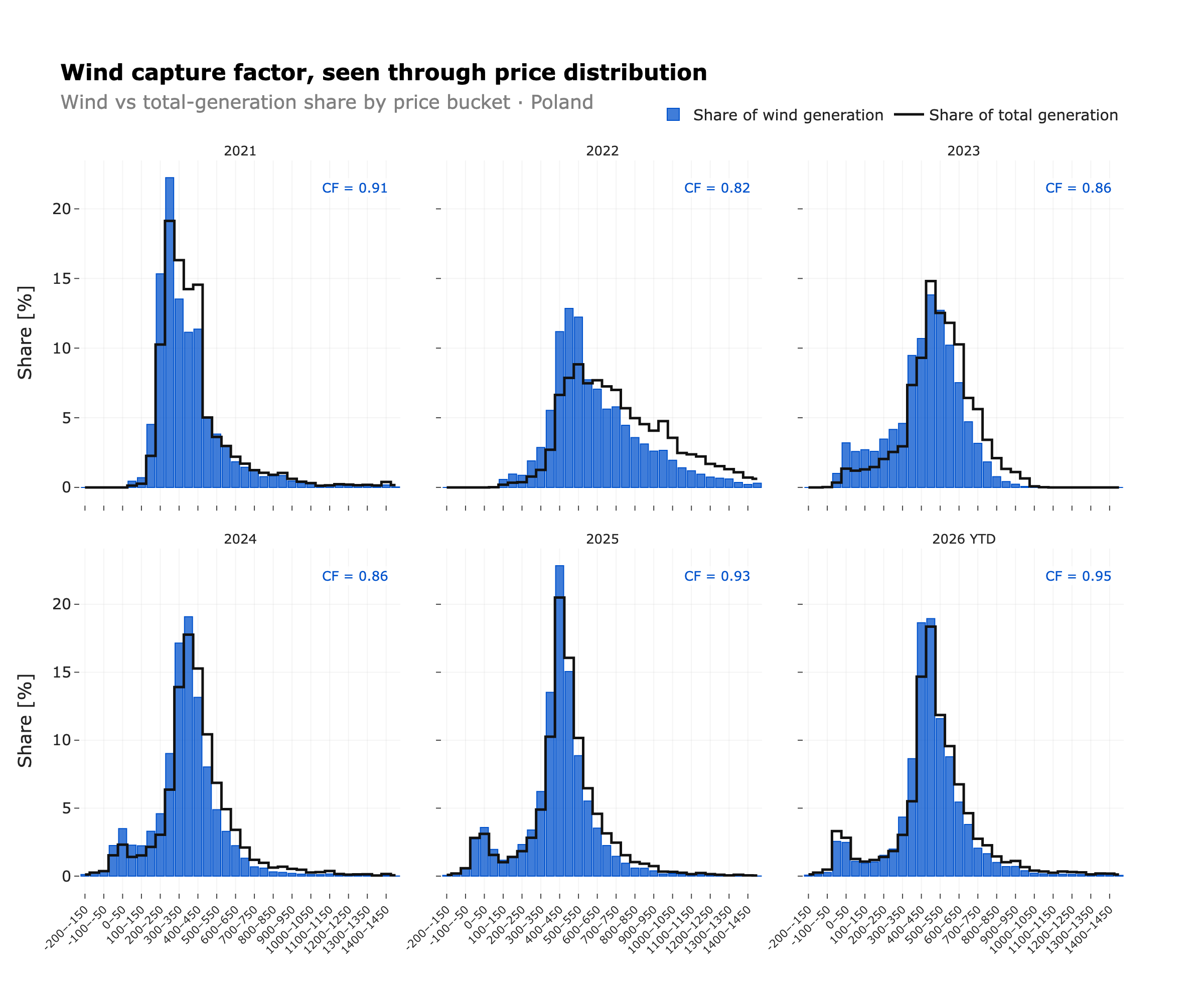

How the lean has evolved year-on-year

These two charts show how the solar and wind distributions have evolved over time. The solar distribution has become more skewed towards low-price buckets, especially in the last two years, while the wind distribution has remained more stable with only minor shifts.

Methodology

Data sources. Generation data from PSE (Polish TSO) and ENTSO-E Transparency Platform. Day-ahead prices from PSE (RCE) — a volume-weighted average of the two DA auctions (TGE fixing I and SDAC).

Gabriel Ziembicki — empirical research on Poland’s energy markets.

* This is revenue, not EBITDA. After land lease, O&M, balancing, insurance, grid fees, curtailment losses, aggregator/PPA margin and debt service, the net cash flow can be materially lower.

More posts

Poland's electricity demand: what temperature and ramps tell us about system stress

Demand in Poland follows a clean two-regime temperature curve with a comfort minimum at 16.5°C and a heating-side slope of 0.213 GW/°C. Residual-load P99 1-hour ramps reached 3.22 GW in 2024–2025 and will likely grow further with PV. A quantitative look at both.

Poland’s solar generation boom and the decline in PV capture factor

As solar generation in Poland grows 10x in five years to 17.5 TWh, capture factors hit record lows of 50%. Exploring the challenges and strategies to keep solar both sustainable and profitable.